Thursday, 18 September 2008

Did the FASB precipitate “the Worst Crisis Since the ’30s?â€

Zachary Karabell has an opinion piece in today’s Wall Street Journal that, if accurate, goes a long way toward explaining how we got to where we are in the current banking crisis. His thesis: It’s “the revenge of Enron:â€

Now I’ll be the first to admit that “I don’t understand all that I know†about this level of accounting. (I have enough trouble keeping my checkbook balanced, and pay somebody else to do my taxes). But I can at least buy this part of his argument, because it make sense: Current value of an asset is relatively meaningless, unless you’re trying to sell that asset right now.

it make sense: Current value of an asset is relatively meaningless, unless you’re trying to sell that asset right now.

Obviously, that isn’t absolutely true (what about your Enron stock, hmmm...?). But haven’t we been told, time and again, that this is the rule behind buy-and-hold investing? You buy on fundamentals, ignore the transient ups-and-downs, and plan on selling out later (often years later) at a nice profit.

So is mark-to-market a bad thing? Karabell spends several column-inches to explain how AIG’s “complex and opaque†business model was difficult to understand, and how the pricing of “derivatives based on derivatives†was even more complex. (To me, that’s a red flag right there: What’s the old saying, “never invest in a business you don’t understand?â€) Then he argues that all this complexity militates against regulation:

Enron deceived investors by pricing its futures contracts artificially high. Today we have all these firms whose assets consist of complex financial instruments that, in compliance with FASB rules, may be priced artificially low. Those instruments will ultimately be worth... what? Is it even possible to predict a current value based on future expectations? When we unwind all the computer models and complex calculations, doesn’t it mean, bottom line, trusting that something is worth what someone else says it is?

Right now the market isn’t trusting any of the numbers, and I defy the “smart people†to write a regulation that would give us numbers that the market would trust. We’re pretty safe in accepting that zero isn’t accurate, but, here and now, what is? And if we’re going fudge the numbers, how can we insure that the fudging we do is equally fair to buyers and sellers (or borrowers and lenders)? Short answers: We don’t know, and we can’t.

Not that there isn’t opportunity...

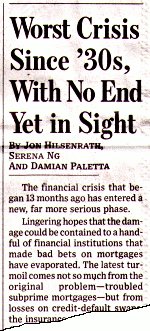

The complete WSJ article:

Comments are disabled.

Post is locked.

Zachary Karabell has an opinion piece in today’s Wall Street Journal that, if accurate, goes a long way toward explaining how we got to where we are in the current banking crisis. His thesis: It’s “the revenge of Enron:â€

The collapse of Enron in 2002 triggered a wave of regulations, ...[including changes in]... accounting rules that forced financial service companies to change the way they report the value of their assets (or liabilities). Enron valued future contracts in such a way as to vastly inflate its reported profits. In response, accounting standards were shifted by the Financial Accounting Standards Board and validated by the SEC. The new standards force companies to value or “mark†their assets according to a different set of standards and levels.

...Beginning last year, financial companies exposed to the mortgage market began to mark down their assets, quickly and steeply. That created a chain reaction, as losses that were reported on balance sheets led to declining stock prices and lower credit ratings, forcing these companies to put aside ever larger reserves (also dictated by banking regulations) to cover those losses.

In the case of AIG, the issues are even more arcane. In February, as its balance sheet continued to sharply decline, the company issued a statement saying that it “believes that its mark-to-market unrealized losses on the super senior credit default swap portfolio . . . are not indicative of the losses it may realize over time.â€...

What AIG was saying then, and what others from Lehman to Bear Stearns to the world at large have been saying since, is that the losses showing up aren't “real.â€

Now I’ll be the first to admit that “I don’t understand all that I know†about this level of accounting. (I have enough trouble keeping my checkbook balanced, and pay somebody else to do my taxes). But I can at least buy this part of his argument, because

it make sense: Current value of an asset is relatively meaningless, unless you’re trying to sell that asset right now. Obviously, that isn’t absolutely true (what about your Enron stock, hmmm...?). But haven’t we been told, time and again, that this is the rule behind buy-and-hold investing? You buy on fundamentals, ignore the transient ups-and-downs, and plan on selling out later (often years later) at a nice profit.

The value of the underlying assets -- homes and mortgages -- declined, sometimes 10%, sometimes 20%, rarely more. That is a hit to the system, but on its own should never have led to the implosion of Wall Street. What has leveled Wall Street is that the value of the derivatives has declined to zero in some cases, at least according to what these companies are reporting.But the current rule requires companies to account for derivatives at those “market†prices, and the companies had signed on to other agreements that relied on the resulting figures. The combination has produced a cascading failure similar to what happened to those who bought stocks on margin just before the 1929 crash: Mousetrapped by a momentary downward spike in prices, they had to sell out, forcing prices (and market confidence) down even more.

There's something wrong with that picture: Down 20% doesn't equal down 100%. In a paralyzed environment, where few are buying and everyone is selling, a market price could well be near zero. But that is hardly the “real†price.

So is mark-to-market a bad thing? Karabell spends several column-inches to explain how AIG’s “complex and opaque†business model was difficult to understand, and how the pricing of “derivatives based on derivatives†was even more complex. (To me, that’s a red flag right there: What’s the old saying, “never invest in a business you don’t understand?â€) Then he argues that all this complexity militates against regulation:

Legislators and agencies would be wary of passing rules regulating how a semiconductor chip is programmed [Ha! Only because they haven’t thought of it yet! -o.g.]; they would recognize that while the outcomes those chips produce might be simple, the way they produce them is not.Karabell obviously has more faith in the wisdom of legislators (and their regulatory-agency minions) than I, but his point that stupid regulation screws up markets remains valid. But as long as the markets are being bailed out with public money, some form of regulation will be there.

Enron deceived investors by pricing its futures contracts artificially high. Today we have all these firms whose assets consist of complex financial instruments that, in compliance with FASB rules, may be priced artificially low. Those instruments will ultimately be worth... what? Is it even possible to predict a current value based on future expectations? When we unwind all the computer models and complex calculations, doesn’t it mean, bottom line, trusting that something is worth what someone else says it is?

Right now the market isn’t trusting any of the numbers, and I defy the “smart people†to write a regulation that would give us numbers that the market would trust. We’re pretty safe in accepting that zero isn’t accurate, but, here and now, what is? And if we’re going fudge the numbers, how can we insure that the fudging we do is equally fair to buyers and sellers (or borrowers and lenders)? Short answers: We don’t know, and we can’t.

Not that there isn’t opportunity...

A few years from now, there will be a magazine cover with someone we’ve never heard of who bought all of those mortgages and derivatives for next to nothing on the correct assumption that they were indeed worth quite a bit.But that “someone we’ve never heard of†will have most likely been risking his own money.

The complete WSJ article:

Posted by: Old Grouch in

In Passing

at

16:52:44 GMT

| No Comments

| Add Comment

Post contains 949 words, total size 8 kb.

74kb generated in CPU 0.0436, elapsed 0.1263 seconds.

51 queries taking 0.1097 seconds, 200 records returned.

Powered by Minx 1.1.6c-pink.

51 queries taking 0.1097 seconds, 200 records returned.

Powered by Minx 1.1.6c-pink.

{kind=link}